VIX

VIX or the Volatility Index was started by CBOE or the Chicago Board of Trade in 1993. It was originally designed to measure the market’s expectation of the implied or expected volatility over the next 30 days on S&P 100 at-the-money options.

Soon it became popular among market participants & it started getting called the ‘Fear Gauge’. In 2003, CBOE again updated VIX to include S&P 500 options.

What is India VIX?

In India, NSE launched India VIX in April 2008. NSE also introduced VIX futures in 2014 but it’s now discontinued because of lack of liquidity.

The Volatility Index is a measure of the market’s expected or perceived volatility over the next 30 days. It’s calculated on the basis of the order book of Nifty options at various strike prices.

VIX shows the expected market volatility over the next 30 days and thus shows us the extent of fear or risk in the market. If VIX is high, then market participants expect the market to fluctuate widely and hence the demand for options to protect the portfolios rises.

Is India VIX Mean Reverting?

It is a well-established fact that the high volatility period is followed by low volatility & vice-a-versa. Therefore VIX also shows mean-reverting characteristics, not always but on most occasions.

Larry Connors of Tradingmarkets.com has done a lot of research on volatility & VIX. What he has found is that VIX is a dynamic indicator & not a static indicator. Also, the VIX is mean reverting in the short term.

In his book, Short Term Trading Strategies that Work, Larry Connors introduced the VIX 5% rule. He found that since the VIX is a dynamic indicator, it makes more sense to look at it in terms of where it was recently rather than a static number. The VIX 5% Rule looks at where the VIX is currently relative to its 10 Day Moving average. If it’s 5% above or below the 10 DMA, it’s probably overstretched on either side and will likely revert to the mean.

Inverse relation to market:

Markets & VIX share an inverse relationship. When the markets are down, the fear rises among the market participants and the VIX also rises. When the markets are rising, there is a sense of greed or complacency in market participants and the VIX falls.

If the VIX rises too far up from its mean, the markets are probably oversold and revert to their mean over the next few days. If the VIX is far below its mean, the markets are likely overbought and will probably correct or go sideways.

We will test this behavior using Larry Connors VIX Rule with one tweak. Instead of using 10 DMA as suggested by Connors, I will use 5 DMA simply because it’s more dynamic. Also, we are looking at the mean reversion tendencies within 3-5 days, 5 DMA fits the bill.

We will apply the following rules on NIFTY 50 from 12-01-2007 till 31-12-19. The rules are applied on spot NIFTY assuming you can buy NIFTY just like any other stock. The idea is to look at what happens to NIFTY when the VIX is overstretched relative to its 5DMA.

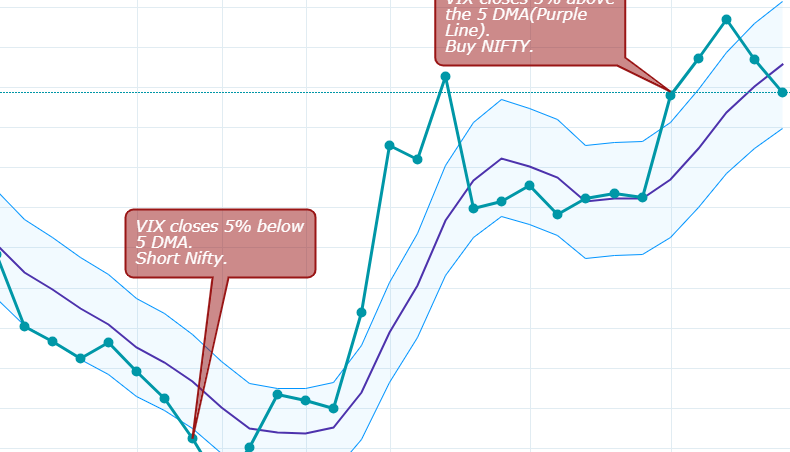

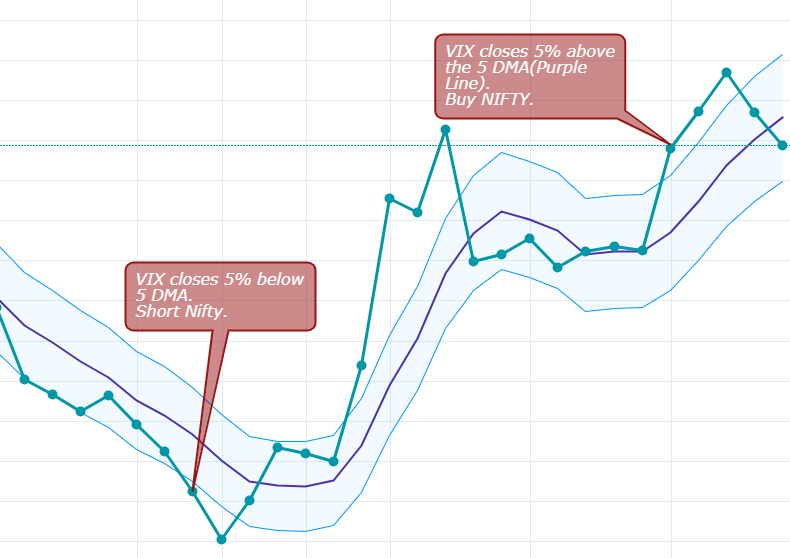

- India VIX closes 5% or more above its 5 DMA.

- The Nifty must be below its 5 DMA.

- If the above two conditions are met, buy on the close.

- Exit on close above 5 DMA.

- Opposite for shorts.

Let’s see below example to better understand the rules…

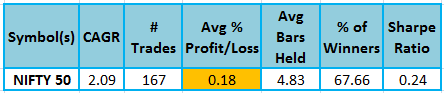

Simple rules… Now let’s see how they perform on NIFTY 50.

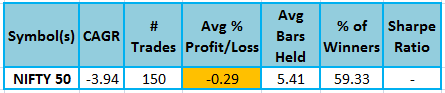

On average nifty rises by just 0.18% whenever India VIX is at least 5% above its 5DMA. Results are positive but not inspiring! Let’s see what happens on the short side.

It loses money on the short side. This is consistent with what I have found that mean reversion strategies don’t work that well on the short side as compared to the long side. Maybe you need different parameters and rules on the short side.

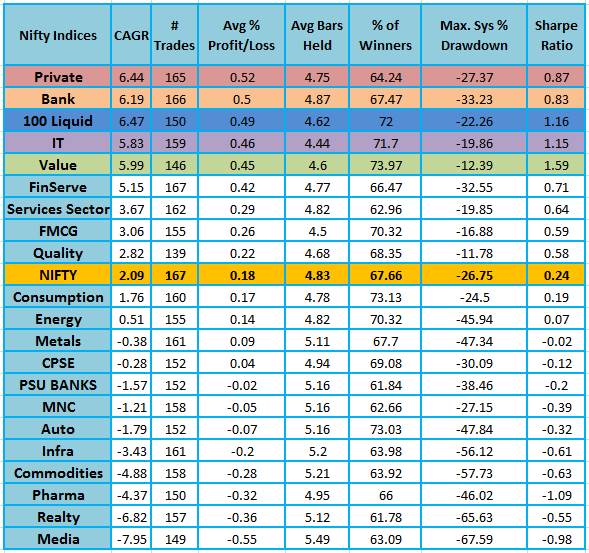

How about other Nifty indices?

Let’s check out what happens to other NIFTY indices like NIFTY BANK, IT, etc when applied the exact same rules on the long side.

As you can see from the table how different sectoral indices behave with respect to VIX. Top 5 performers in terms of average gains are highlighted.

Why do these 5 sectoral indices do better in relation to the VIX? Well, my guess is, when there is heightened volatility in the market, people look for safe sectors and stocks like IT & private sector large companies including large private banks.

By the same token, when the volatility is high, sectors like Media, Real estate, Infra, and Commodities perform badly. Market participants are looking to exit high volatility, high levered stocks and park money in safe, low volatility stocks as evident from the above table.

But one interesting observation is that the NIFTY VALUE outperforms all other sectors in terms of higher Sharpe ratio, Higher win rates, lower drawdown & reasonably higher average gains. Why?

Again my guess is ( and a guess is just that, a guess) when VIX is far above its mean, markets are probably oversold & so are the value stocks forming part of the NIFTY 50 VALUE 20 index. Market participants are likely getting value stocks at a bargain price which lifts up the index over the next few days.

Nifty Bank also has a great performance because 1) Higher VIX shows that there is a high volatility environment in the market and 2) Nifty Bank itself is highly volatile and 3) the previous both factors are conducive to mean reversion strategies. Simply stated mean reversion works best in a high volatility environment and thus on NIFTY BANK.

How can you apply this system?

There are many ways you can apply this knowledge.

There are many ETFs available on these indices on NSE. Probably you can trade this system on Nippon NV20 ETF, BANK BEES, etc.

But the best way to profit from this strategy is Options, particularly Bank Nifty options. There are three possible scenarios that occur when VIX is overstretched…

- The markets are probably oversold.

- The option prices are inflated, especially put options because market participants are rushing to protect their portfolios by buying puts.

- Both the VIX & market will revert to their mean as we saw in the above tests.

Keeping the above three scenarios in mind, it makes sense to have an option strategy where you receive the premium credit. Buying already inflated options is not a great strategy in this scenario. So the simplest strategy would be credit spreads and specifically Bull Put Spread.

What is Bull Put Spread? It is a credit positive strategy where you sell OTM puts and buy further OTM puts to protect the downside. You can keep the net premium when the VIX reverts to its mean.

Exact strategy is beyond the scope of this article but we will test it out in future posts.

What about stocks?

Can this system be applied to direct stocks? Let’s find out.

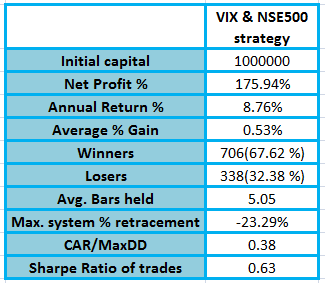

The same system will be applied to stocks from NSE 500. When we are applying the system on stocks, we must define the rules again…

- Close is above 200 DMA.

- India VIX closes 5% or more above its 5 DMA.

- Stock must be below 5 DMA for at least 3 days & today’s close must be lower than the previous close.

- When all the above 3 conditions are met, Buy on the close.

- Exit when the stock closes above its 5 DMA.

- Maximum 5 positions at 20% each allowed.

- Rank stocks in terms of the most oversold based on RSI2.

Let’s see how the system fares on stocks.

This simple strategy delivers an annualized returns of around 8.76% with a maximum peak to valley drawdown of around -23%. Not bad for a simple system like this.

The VIX 5% rule can be applied to stocks as evident from the test result.

Conclusion:

- As generally expected that India VIX & Nifty have an inverse relationship. That is true to some extent but not with a wide margin. As we saw from the above test, Nifty does poorly as compared to other indices. Maybe because Nifty has more trending characteristics than mean reversion. Again I have seen many mean reversion strategies do not produce great results when applied on Nifty. We will try to explore this behavior in future posts.

- India VIX 5% rule works very well on NIFTY Private Sector, Nifty Bank, Nifty 100 Liquid 15, NIFTY IT and NIFTY 50 Value 20.

- India Vix 5% rule works better on the long side as compared to the short side. Option strategies probably could work but that has to be tested.

- Trading options strategies would be a great way to profit from India VIX 5% rule. But option contracts are only available in NIFTY BANK & NIFTY IT. It makes sense to trade options strategies like credit spreads on NIFTY bank as NIFTY IT is not that liquid.

- You can apply this system on direct stocks with additional filters. Maybe you can implement option strategies on the stocks belonging to the high performing indices like Nifty bank, Nifty 50 Value 20, NIFTY IT, etc.

*** Actual results may significantly vary from historical results. Past performance may or may not be sustained in the future. Survivorship bias exists. This is not investment advice and is only for illustration, information & educational purposes. Please read Disclaimer before making any purchase.

Very thought provoking analysis.Thanq very much Sir

Thanks 🙂